The Coming Train Wreck for Older Workers

A warning from a new survey on retirement expectations

Uh-oh.

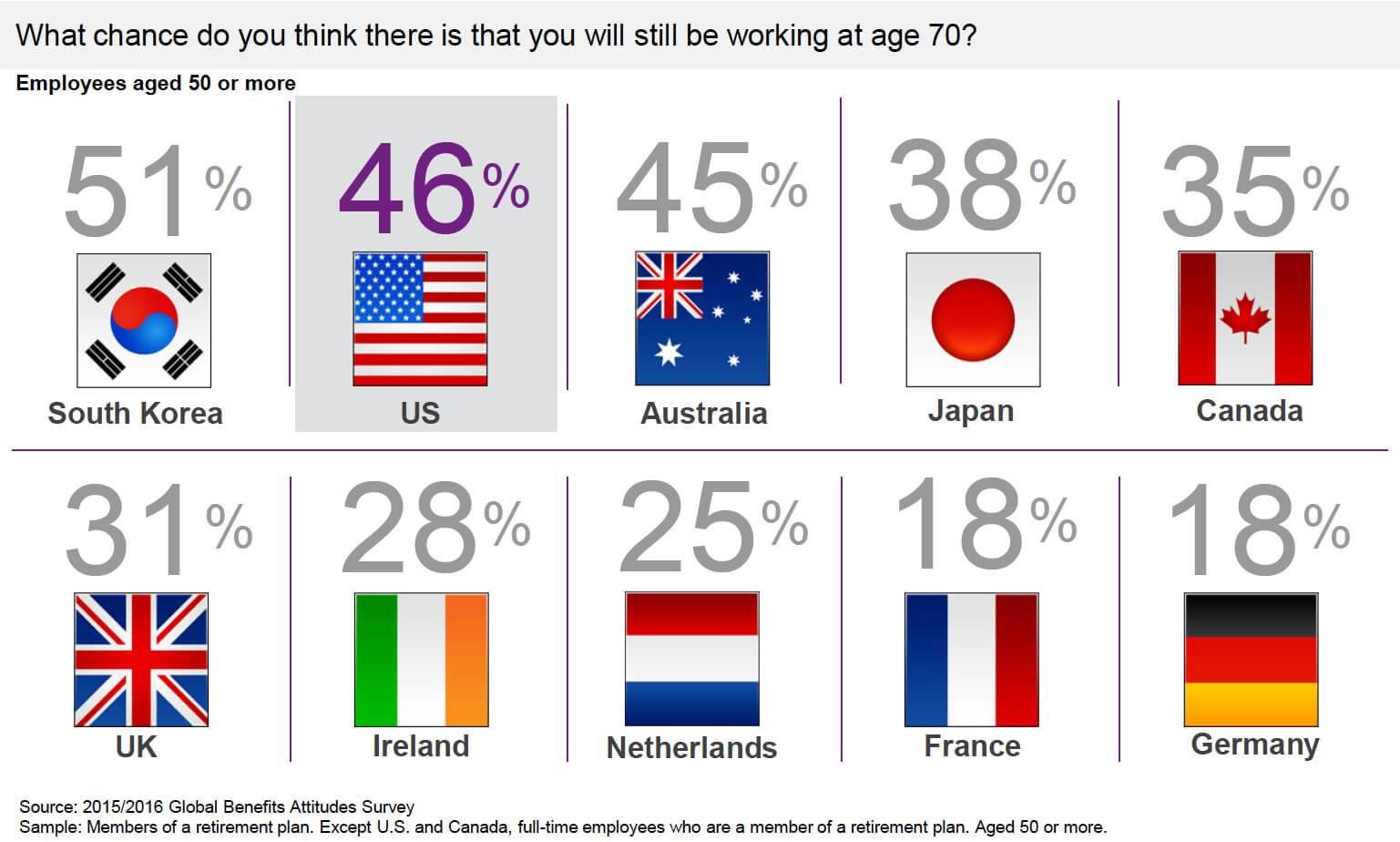

American workers aged 50 or older think there’s nearly a 1 in 2 chance they’ll still be working at 70 (see chart below), but many employees who expect to work longer are exactly the ones who’ll likely be least able to do so.

That’s the upshot of the new, frightening (for employees and employers) 2015/2016 Global Benefits Attitudes Survey by Willis Towers Watson, a global benefits advisory consultant. The firm surveyed 5,083 U.S. employees at large companies, as well as roughly 25,000 employees in 18 other countries.

The workers expecting to keep plugging away until 70, the study discovered, are often “the most vulnerable” and “showing higher levels of stress, lower levels of health and lower levels of engagement with their current jobs,” says Shane Bartling, senior consultant at Willis Towers Watson.

“That’s an uncomfortable fact for employees facing a very difficult situation and it sends a warning sign to employers about what’s transpiring in the new retirement system in the United States that we’ve put in place,” Bartling adds.

The Survey Says...

According to the survey, of those planning to retire after 70:

- Only 47 percent say they are in very good health

- 40 percent feel they are stuck in their jobs (compared with 27 percent who plan to retire before 65)

- 40 percent have high or above average stress (compared to 30 percent of those expecting to retire at 65)

- 48 percent of workers earning below $35,000 expect to work to 70 or later (vs. 20 percent of those making $75,000 or more)

And if these vulnerable workers find themselves out of work, but wanting to be employed, the psychological effects — not to mention the financial ones — could be devastating.

As New School economist Teresa Ghilarducci just wrote, according to the government’s Health and Retirement Study of older Americans, “unemployed respondents were more likely than both workers and retirees to report a general feeling of helplessness. Among 55- to 64-year-olds, 40 percent of the unemployed agreed with the statement, ‘I often feel helpless in dealing with the problems of life.’” By contrast, only 8 percent of retirees and 16 percent of older workers felt that way.

Bartling worries (as do I) that many of the older, vulnerable workers have meager retirement savings and “don’t have options.” The question, says Bartling, “is how are they going to be able to continue working?”

Painful Decisions Ahead

And how will this play out for them? “These employees may be confronted with very painful decisions around having to adjust their lifestyle expectations in retirement and fall back on family and the social safety net in a bigger way than they had hoped,” says Bartling.

I’d like to see more employers taking more action to prevent this coming train wreck. It’s true that growing numbers of firms — especially large ones— are offering financial wellness and physical wellness programs, which is reason for some optimism.

Last year, a survey of 250 employers by the Aon Hewitt benefits consulting firm, said 93 percent of those firms planned to focus more on financial wellness for employees in ways extending beyond retirement decisions. Aon Hewitt’s Director of Retirement Research, Rob Austin, called financial wellness ‘sort of The Next Big Trend’ in benefits. Says Bartling: “We’re certainly seeing an increase in the attractiveness of financial planning support.”

Exactly how much good financial wellness programs do, however, is an open question, since the programs vary dramatically in how they work and who participates in them. “Many of those programs struggle to fully engage employees and get desirable outcomes,” says Bartling. “Now, the emphasis is on how to amplify those interventions, akin to financial biometrics.”

The success of physical wellness programs at work has been a mixed bag, too. Although 81 percent of larger companies now offer physical wellness programs, according to a 2015 survey by the Kaiser Family Foundation, health writer Sharon Begley recently wrote on the excellent Stat website that “there is a startling lack of rigorous evidence that they achieve their stated goals.”

But Bartling says: “It’s incumbent for all employers to understand how extensive [financial stress] is in the workforce. That’s only just beginning to happen.”

The State of Retirement Unreadiness

I asked Bartling whether he thinks many workers really will need to hold down jobs until after 70, as one in four expect. “We’ve done retirement readiness analysis for nearly 100 employers in the United States and the statistics based on that are not dissimilar from the results in the employees survey,” he says.

However, Bartling adds, there’s a “wide distribution of retirement readiness within the workforce.” And no, it’s not that wealthier workers are necessarily better prepared financially than lower-income ones.

“Many employees at both ends are well-prepared and underprepared,” says Bartling. “There are many situations where higher-paid employees actually have a higher level of a lack of preparedness,” due to living beyond their means.

One other notable finding in the new Willis Towers Watson survey: The percentage of Americans who expect to retire after age 65 has fallen from 52 percent in 2013 to 46 percent now. That, Bartling says, is likely a reflection of the improving economy.

But the next recession will come sometime, so that falling percentage is likely to head right back up again when times get tougher.