Where Older Adults Are Most Financially Insecure

The cities and communities probably aren't ones you'd expect

When most of us (and retirement experts) think about how prepared we'll be for a financially comfortable retirement, it's typically about how much money has been saved for it. But University of Massachusetts Boston professor Jan Mutchler says there's another way to look at it: Will you have enough income to afford the local cost of living?

Based on the number-crunching that Mutchler and her Gerontology Institute at U Mass Boston colleagues have done creating what's known as the Elder Index, the answer for millions of Americans is, sadly, no.

"When we focus on older people living alone nationwide, about half do not have income sufficient to cover the cost of living in the location where they live."

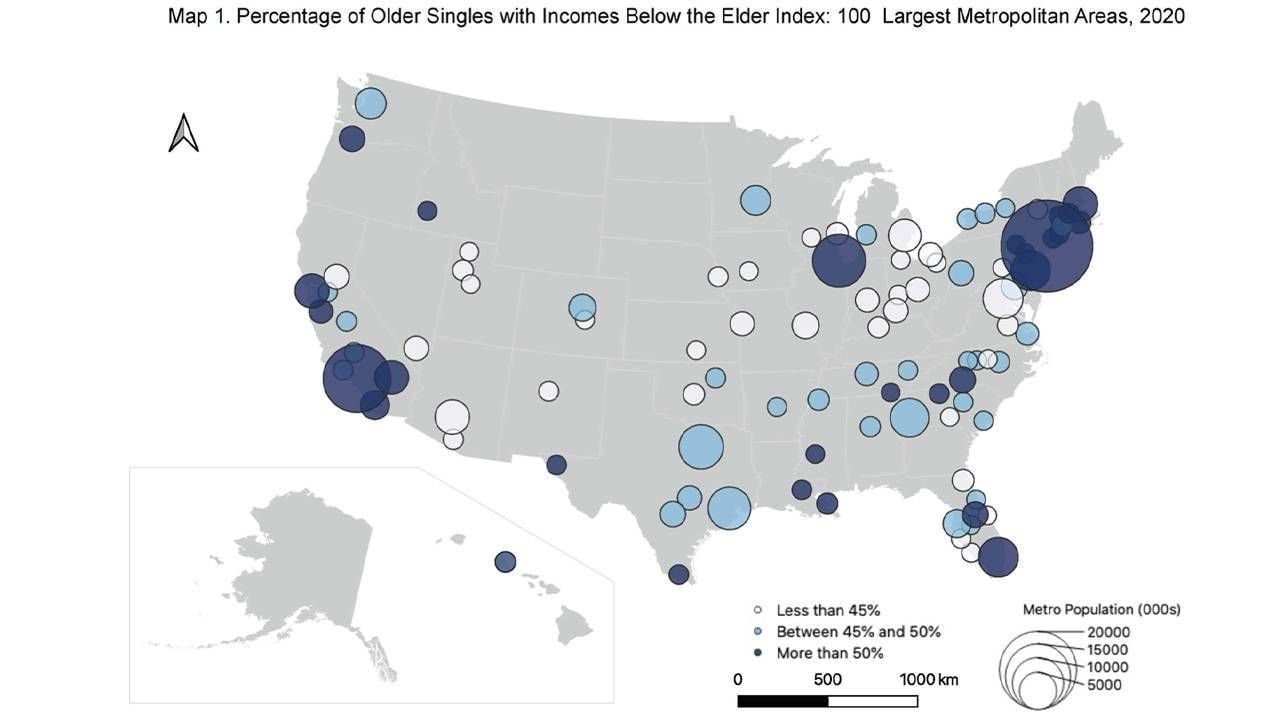

Mutchler's recent study ("Aging in the 100 Largest Metropolitan Areas: How Do Older Adults Fare?") found that in each of the 100 biggest U.S. metros, at least 37% of single residents age 65 and older and at least 12% of older couples are at risk of being unable to afford basic needs and age in their own homes.

But things are much worse in certain places, where at least 60% of older singles and 40% of older couples face this economic insecurity, Mutchler found. (Her team has Elder Index numbers for each of the nation's 384 metro areas on the Elder Index site.)

And these numbers don't account for the potential cost of long-term care, which can be exorbitant. The HealthView Services research and consulting firm now estimates that eventual long-term care costs for an average healthy 65-year-old woman would be $373,712 and for a man, $237,368 (excluding Medicare premiums and co-pays).

I spoke with Mutchler about where older Americans are most economically insecure and why, and about what could be done to help:

Next Avenue: What is the Elder Index and how it is created?

Jan Mutchler: The Elder Index is essentially a cost of living measure for older adults, and it's meant to be a threshold to indicate what people need to get by and remain independent in their community.

They wouldn't be able to go on a vacation or to give a lot of money to their children or their grandchildren, but they would be able to stay in their home.

And how do you compile the numbers?

We're looking at government survey data about how much people actually spend on housing and for health care. Then we have a survey based on how much older people who don't work need to drive to get their business done on a daily basis. We have food information, and a small additional amount that is meant to cover basic things. We then calculate those values for different areas in the country.

And tell me what the purpose is. Why create an Elder Index?

We were looking for something that would convey a sense of where people stand with respect to their retirement resources and whether continuing to work might be beneficial for them.

What is the Elder Index showing now in terms of economic security or insecurity across the country in general?

Well, across the country in general, it shows that it costs much more than would be suggested by the poverty line to get by. It also costs more than people get from Social Security.

In every area, no matter what county you're looking at or what state or metro area, the Elder Index is higher than the average Social Security benefit. So it makes very clear that people can't live on Social Security alone.

And when we focus on older people living alone nationwide, about half do not have income sufficient to cover the cost of living in the location where they live. So, it suggests that there's a lot of people struggling out there.

What did you find when you looked at the hundred largest metro areas?

Some of the very largest areas are extraordinarily expensive: a number of metro areas in California; most of the metro areas in the Northeast — like Boston and New York City. They have large shares of people who fall below the Elder Index. Chicago is very high. There are locations in Florida as well. It's clear that living expenses are very high in these areas.

But the very highest share of people falling below the Elder Index is actually in McAllen, Texas. Another is El Paso. Those are areas where the cost of living isn't particularly high. And yet you see very high shares of people falling below the index.

Clearly, what's happening there is you've got very low incomes.

So elder economic insecurity isn't necessarily highest in places with the highest cost of living. Right?

Exactly.

And were there particular places that surprised you, where you didn't think it would be so difficult for people to live? Or ones where you thought there would be a higher percentage of people having economic insecurity issues than actually did?

I will say that those Texas border areas really did surprise me. It is stunning to see the high poverty rates there and the high share of people falling below the Elder Index.

"I think our work with comparing the Elder Index to Social Security suggests that Social Security levels are too low."

I'm in Massachusetts and I was distressed to see, frankly, that really all of the Massachusetts metro areas are quite high in terms of the share of people living below the Elder Index.

I know that people with very low incomes in Massachusetts are eligible for government services or non-cash supports that may help them bridge the gap. And those supports may not be in place in some other parts of the country.

In many states, these benefits are not as generous as they are in Massachusetts and in some other areas.

What are examples of these services and supports?

In some communities and states, there's a lot more subsidized housing or more generous nutrition programs or just more opportunities to take advantage of nutrition services that can offset food costs.

A lot of states and communities have benefits helping people pay for their utilities or their property taxes.

So, there are a lot of programs that do exist, but people need to know about them, and they need to be able to access them.

If I'm in my fifties or sixties and I'm thinking about where I'm going to want to live in retirement, how should I look at the Elder Index in making that determination?

We hear from a lot of people that they use the Elder Index that way; people who are very systematic about wanting to think about how to make their retirement funds go the farthest. I think the Elder Index can be useful for that.

I think considering what kind of programs or benefits might be available, that's an important thing for people to do.

There are a lot of things that go into where people live, but the Elder Index, I think, can be one of those.

Let's say I would like to know whether an area I'm thinking about moving to offers any services and supports. Is there an easy place to go, either locally or nationally, to get that information? Do you go to the Area Agency on Aging?

The place that would be most consistent across the nation to work would be the Area Agencies on Aging. The National Council on Aging has a lot of great resources on its site, too.

Based on your work, do you think that that federal, state or local policies should change to address economic insecurity, particularly in places like McAllen, Texas? And if so, what would you like to see them do to be more helpful?

I think there's a lot that could be done. And I do think something needs to be done.

I think just the fact that half of Americans living alone at age sixty-five or over have incomes below the Elder Index, incomes that don't really support remaining healthy and stable in their own homes — that issue alone suggests that something needs to be done.

I think our work with comparing the Elder Index to Social Security suggests that Social Security levels are too low. At the federal level, it certainly speaks to continuing to support or raise support for Medicare to help older people pay their health expenses.

There's a lot that can be done around property taxes — like tax deferrals and tax waivers to help protect seniors' quality of life.

What about in terms of long-term care costs? Is there anything you'd like to see done to help older people with high long-term care costs where they live?

The Elder Index does not factor in any long-term care costs. The really extraordinary thing about those expenses is that they very quickly can double your living expenses.

The fact that most long-term care is provided by family members, causing some of them to leave the workforce early or experience financial problems for themselves, speaks to that. Clearly, long-term care is something that needs to be addressed, I think, at the federal level as well as at the state level.