Prosperity in America? Not for Low-Income People

The troubling numbers in the 2018 Prosperity Now Scorecard

(Editor’s Note: This story is part of a partnership between Next Avenue and Chasing the Dream, a public media initiative on poverty and opportunity.)

In his State of the Union address, President Trump said “there has never been a better time to start living the American Dream.” But the new 2018 Prosperity Now Scorecard and its accompanying report says that isn’t so for low-income Americans.

“The system is, by just about all measures, stacked against those with low-incomes and low wealth for the benefit of the wealthiest,” says the report from the nonpartisan but left-leaning Prosperity Now nonprofit, which provides research and recommendations regarding Americans with limited incomes.

One example: low-income people are ineligible for federal programs such as SNAP (food stamps) and TANF (Temporary Assistance for Needy Families) if they amass “even modest savings,” the report noted. Prosperity Now calls policies like this “a roadblock on the path to saving.”

What the 2018 Prosperity Now Scorecard Found

The 2018 Prosperity Now Scorecard and its report, Whose Bad Choices? How Policy Precludes Prosperity and What We Can Do About It, also make the argument that the U.S. economic system and policies of the Trump administration and Congress are stacked against people of color.

“We’ve heard more rhetoric lately about [low-income] people making ‘bad choices’ or being ‘irresponsible with money’ and that’s been the direction policy has been going,’ said Kasey Wiedrich, director of applied research at Prosperity Now. “We wanted to attack that.” One example of the rhetoric: Sen. Chuck Grassley (R-Iowa) recently said lower-income Americans “are just spending every darn penny they have whether it’s on booze or women or movies.”

In reality, however, the Prosperity Now report said, “the dominant narrative about low-wealth people is nothing but a series of myths.” Poor choices, the analysts there say, aren’t why people are poor.

The 2018 Prosperity Now Scorecard reviewed 115 outcome and policy measures for all 50 states and the District of Columbia to see how well residents are faring in five categories, and how much progress each state has made in adopting policies in them “toward building a path to prosperity for all its residents.” The categories: financial assets and income; businesses and jobs; homeownership and housing; health care and education.

Best and Worst States in the Scorecard

The top five states, starting with the best: Vermont, New Hampshire, Hawaii, Minnesota and Utah. The bottom states, starting with the worst: Mississippi, Louisiana, Georgia, Nevada and New Mexico and Alabama, which tied.

Wiedrich said the states with the lowest Scorecard rankings typically have “the highest rates of low-wage jobs, lower credit scores and households struggling with incomes.” Also, she added, these states tend to “have less of a safety net.” As a result, “a financial emergency may hit their residents harder.”

Low-wage jobs are a chief reason so many low-income Americans have trouble making ends meet these days, according to Wiedrich.

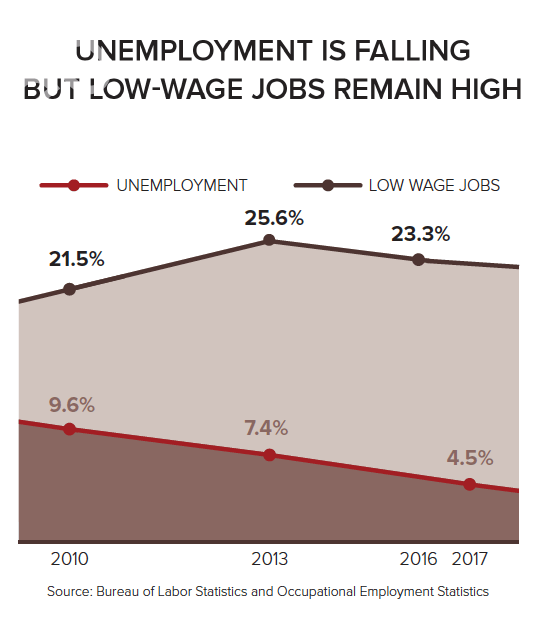

This year’s Scorecard found that nearly one in four jobs are in low-wage occupations — ones that don’t pay enough to keep families above the federal poverty line. And, Prosperity Now’s researchers say, even though unemployment has been cut in half since its peak in 2010 (from 9.6 percent to 4.5 percent), the rate of low-wage jobs has decreased by just two percentage points since 2013 (to 25.6 percent) and is still higher than in 2010 (when the rate was 21.5 percent).

Weidrich concedes that “there’s been an incremental improvement in a lot of economic measures compared to a year ago.” In addition to the falling unemployment rate (just 3.0 percent for people 55+), there are the rising stock market (until the past few days), increasing wages — up 2.9 percent in the past year — rising median net worth and a drop in the number of Americans without health insurance (something which may change with the repeal of the Affordable Care Act mandate).

Some Economic Improvements, But 'Not a Panacea for All'

But, Wiedrich is quick to add, “it’s still not a panacea for all.”

Although the median net worth has been rising more for people of color than for whites, the unemployment rate is still more than twice as high for Blacks (7.7 percent) than for whites (3.5 percent).

And roughly half of renters (46 percent of white renters and 54 percent of renters of color) are what Prosperity Now calls “cost-burdened” — they spend more than 30 percent of their income on housing costs. “That lowers their ability to save to buy a home,” said Wiedrich. “The homeownership figure in America has not really moved.”

Prosperity Now argues that the 2017 tax law and a wave of deregulation by the Trump administration and Congress are helping the wealthiest Americans and corporations far more than people with low incomes.

The group’s report cites a Tax Policy Center estimate that the new tax law will translate to a $51,140 tax cut for the wealthiest 1 percent of households, but families earning less than $25,000 in 2018 will see “a mere $60 in tax savings.” House Speaker Paul Ryan (R-Wis.) just took heat for tweeting about a Pennsylvania high-school secretary who was pleasantly surprised her paycheck rose $1.50 a week due to the tax cut.

What the Prosperity Now report doesn’t mention, however, is that the new tax law also doubled the standard deduction (to $24,000 for married couples filing jointly) and doubled the child-care tax credit (to as much as $2,000 per qualifying child). Both changes stand to help low-income Americans.

What the Debt Figures Say

For the first time, this year’s Prosperity Now Scorecard included data on Americans’ levels of personal debt and their debt management. Both have been improving, overall — but there are a few debt trends going in the wrong direction.

On the plus side, median credit card debt fell 6.5 percent from $2,397 in the second quarter of 2010 to $2,241 in the second quarter of 2017, adjusted for inflation. And the percentage of consumers with delinquent credit card debt decreased from 11.7 percent of borrowers in 2010 to 8.4 percent in 2017.

But student loan debt is a growing problem: Median student loan debt increased by 21.4 percent between 2010 and 2017, from $14,588 to $17,711. The percentage of student loan borrowers who are delinquent (15.8 percent) is nearly twice the percentage of delinquent credit card borrowers. Among those over 55 with student loan debt, 12.3 percent are severely delinquent.

Also, the report noted, many households of color are dealing with debt issues. “Student loan debt typically haunts students of color for much longer than other students,” it said. Households of color are also more likely to be turned down for loans and are more vulnerable to fees and predatory products than white households.

An Urban Institute study of 60 U.S. cities discovered that the predominately white areas had a median credit score 80 points higher than in predominately non-white neighborhoods, which can cost families of color $100 or more each month on a mortgage. And the Federal Reserve Board’s Survey of Consumer Finances found that African American households are twice as likely as white household to be late on credit payments.

All in all, Wiedrich said, Americans with low wealth generally aren’t reaping the benefits of today’s humming economy. Their wages aren’t keeping up with the rising costs of housing and health care. Also, "many are dealing with income volatility, which makes it hard to plan and to make ends meet,” said Wiedrich.

States Expanding the Earned Income Tax Credit

A few states, however, have recently adopted policies — or are working to do so — that could help low-income people on the path to prosperity.

For example, Hawaii, Montana and South Carolina established state earned income tax credits; California and Illinois expanded their credits to cover more working families. These tax credits, like the federal anti-poverty one, put money in the pockets of low- and moderate-income working people so they can keep more of what they earn. Currently, 29 states have a state earned income tax credit.

Helping Americans Save for Retirement

And, although the Trump administration and Congress recently made it tougher for states to set up retirement plans for residents whose employers don’t offer them — a “short-sighted” policy, Weidrich said — a few states are creating them anyway.

California, Connecticut, Illinois, Maryland and Oregon have done this; Massachusetts, New Jersey, Vermont and Washington, the Prosperity Now report said, “are pursuing similar strategies.” That could be especially helpful for low-income people; 77 percent of the lowest-earning workers lack access to an employer-provided retirement plan.

'Lifting Citizens to Prosperity'

President Trump declared in his State of the Union speech that “we can lift our citizens… from poverty to prosperity.” But, Prosperity Now maintains, to make that happen, more states and federal policymakers need to do more — especially now, when times are good for so many.

“At some point, the economy will encounter another downswing or recession and those who are not benefiting much from today’s economic gains will be hardest hit,” said Wiedrich.

This story is part of our partnership with Chasing the Dream: Poverty and Opportunity in America, a public media initiative. Major funding is provided by The JPB Foundation. Additional funding is provided by the Ford Foundation.